How Cross-Border B2B Payments Are Changing in 2026

Cross-border B2B payments have been the most expensive and least efficient part of the global financial system for decades. Settlement takes two to five days. Fees compound through intermediary banks, FX markups, and compliance charges. And trapped liquidity from slow settlement costs the global economy an estimated $120 billion annually according to Gitnux research.

That is changing in 2026. The cross-border payments market is projected to reach $238 billion according to Mordor Intelligence, but the real story is not market size, it is the fundamental rewiring of how money moves between businesses across borders.

Key Takeaways

- Real-time cross-border settlement is moving from pilot to production

- Stablecoins are becoming a legitimate B2B settlement rail

- Modern payment rails cut cross-border costs by 60% or more

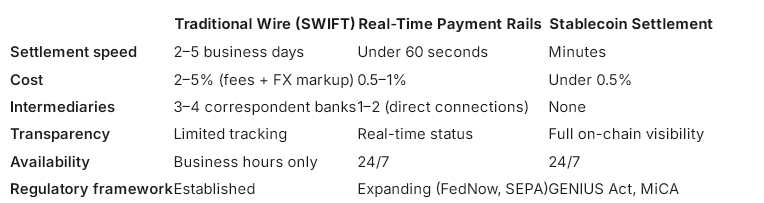

Traditional vs. Modern Cross-Border Payment Rails

Before diving into what is changing, it helps to see the gap between the old model and the new one side by side.

The direction is clear. Every metric that matters to finance teams, speed, cost, transparency, and availability, favors the newer rails.

The Correspondent Banking Model Is Breaking Down

The traditional architecture relies on correspondent banking, a chain of intermediary banks routing payments across jurisdictions. Each link adds time, cost, and opacity. A payment from New York to São Paulo might pass through three or four intermediaries, each taking a cut.

This model does not work for an economy where 95% of businesses engage in cross-border trade and B2B volumes are projected to grow from $39 trillion in 2023 to $56 trillion by 2030.

According to PYMNTS research, 70% of U.S. firms experience higher failed payment rates in cross-border than domestic transactions. Faulty cross-border payments cost U.S. merchants at least $3.8 billion in lost sales annually. And 62% of SMEs report delays and additional costs from navigating more than 190 regulatory regimes worldwide.

Real-Time Payment Rails Are Going International

The most visible change in 2026 is the expansion of real-time payment networks beyond domestic borders. What started as country-level systems, FedNow in the U.S., SEPA Instant in Europe, UPI in India, is now connecting internationally.

The PayNow-UPI bridge between Singapore and India processed $1.2 billion in transactions in 2025. Canada's Real-Time Rail went live in 2026 with instant links to U.S. clearinghouses. SEPA Instant's planned removal of the €100,000 per-transaction cap is expected to unlock significant corporate adoption across Europe. And the BIS Innovation Hub's Project Nexus is working to connect domestic systems globally, targeting settlement within 60 seconds.

For companies managing global supply chains and vendor payments, real-time settlement eliminates the float that has historically trapped working capital for days.

Stablecoins as B2B Settlement Infrastructure

While real-time payment networks connect existing banking systems, stablecoins bypass correspondent banking altogether.

Stablecoin transaction volumes hit $33 trillion in 2025, a 72% increase year-over-year according to Bloomberg and Artemis Analytics. USDC processed $18.3 trillion and USDT processed $13.3 trillion, controlling over 95% of the market. B2B stablecoin payment volumes surged from under $100 million monthly in early 2023 to over $6 billion by mid-2025, as tracked by Stablecoin Insider.

The regulatory foundation now exists. The GENIUS Act requires 100% reserve backing, AML programs, and regulatory oversight for payment stablecoin issuers. The EU's MiCA regulation establishes parallel requirements. These frameworks moved stablecoins from compliance gray zone to regulated financial instrument.

"Cross-border B2B payments are where stablecoins stop being a crypto story and start being a finance story," said Chiara Munaretto, Co-Founder and Managing Partner of Stablecoin Insider. "When a company can settle a six-figure supplier invoice in minutes instead of days, at a fraction of the cost, with full transaction visibility, that is not a speculative bet on digital assets. That is better infrastructure."

For cross-border B2B payments, the advantage is straightforward: settlement in minutes, a fraction of the cost, and full transparency.

AI Is Reshaping Compliance and Fraud Prevention

Cross-border B2B payments generate enormous compliance complexity. Sanctions screening, AML checks, KYC verification, and regulatory reporting across jurisdictions create overhead that slows payments and inflates costs.

AI is now embedded in the compliance workflow as a real-time infrastructure layer. Machine learning models handle sanctions screening, transaction monitoring, anomaly detection, and automated reconciliation simultaneously. AI-driven fraud detection is predicted to save the cross-border payments industry $10 billion annually by 2026 according to ACI Worldwide.

For B2B payments, where transaction values are higher and compliance stakes greater, this automation reduces the manual review bottleneck that has historically added days to settlement.

What This Means for Growing Companies

Companies paying international suppliers, contractors, or subsidiaries now have real alternatives to the wire-and-wait model. When evaluating the best international payment methods, businesses should consider factors such as settlement speed, transaction costs, regulatory compliance, and recipient preferences. Modern payment infrastructure gives companies more flexibility than ever before to optimize cross-border transactions. Real-time payment bridges offer speed within connected banking networks. Stablecoin rails offer speed and cost reduction outside traditional banking entirely. And hybrid platforms combining fiat, stablecoin, and multi-currency capabilities give finance teams the flexibility to optimize by cost, speed, and recipient preference.

The companies moving fastest are in technology, fintech, and e-commerce, sectors where payment velocity directly affects operational efficiency and talent retention. The question is no longer whether cross-border B2B payments will change. It is whether businesses are positioned to benefit from the infrastructure replacing the old model.

FAQs:

1. How are cross-border B2B payments changing in 2026?

Cross-border B2B payments are shifting from slow, expensive correspondent banking networks toward real-time payment rails, stablecoin settlement, and AI-driven compliance automation. Settlement times are dropping from days to minutes, and costs are falling from 2–5% to under 1% on modern infrastructure.

2. What role do stablecoins play in cross-border B2B payments?

Stablecoins like USDC and USDT serve as settlement rails that bypass traditional correspondent banking. With $33 trillion in transaction volume in 2025 and regulatory frameworks in place through the GENIUS Act and MiCA, stablecoins are used for supplier payments, treasury management, cross-border payroll, and intercompany transfers.

3. How much do cross-border B2B payments cost?

Traditional wire transfers cost 2% to 5% in combined fees including FX markups, intermediary bank charges, and compliance processing. Real-time payment networks cost 0.5% to 1%, and stablecoin settlement reduces costs further by eliminating intermediary banks entirely.

4. What is the GENIUS Act and how does it affect cross-border payments?

The GENIUS Act, passed in July 2025, is the first comprehensive U.S. regulatory framework for payment stablecoins. It requires 100% reserve backing in high-quality liquid assets, anti-money laundering programs, and federal or state regulatory oversight, enabling companies to use stablecoins for cross-border B2B payments within a clear compliance structure.

5. What are real-time cross-border payment networks?

Real-time cross-border payment networks connect domestic instant payment systems internationally. Examples include the PayNow-UPI bridge between Singapore and India, Canada's Real-Time Rail linking to U.S. clearinghouses, and SEPA Instant across Europe. These networks enable settlement in under 60 seconds.